Unleash the sexiness of Money Market Fund

- Hotcup

- Feb 9, 2021

- 6 min read

Updated: Feb 10, 2021

Things you should know about Money Market Fund and how it can benefit us

I believe money market fund (MMF) is a new term to many of us including myself. Ever since kicking start with my personal finance journey, I have always been searching for weapons to combat against the silent killer of our finances – Inflation.

Alright I’d to admit MMF might not be a formidable weapon, perhaps to add some visual I would say it serves as a sturdy shield to help us fend off inflation. Let’s see how this new term can benefit us.

What is a money market fund (MMF) and how it works?

A money market fund invests in high quality and short-term cash equivalent instruments, commonly known as “money market instruments”. Money market funds serve as a middleman to pull money from investors and lends money to banks (banks treat it as a way to shore up short-term cash to make up for its daily deposit reserve shortfall) to earn returns. As they are backed by the banks, these instruments are considered very low risk.

Besides, a MMF holds fixed deposits from banks as another way to earn their return. This is because MMFs have a network of banks that they can easily tap into to find the best rates, coupled with their high negotiating power (in contrast to retail investors ☹) as they can place large amounts of money, often up to a few hundred million dollars, with the banks.

The money market isn’t directly accessible to retail investors because of the large amount of money transacted in the market on a daily basis. But by investing in a MMF, we can easily obtain exposure to the money market as a small retail investor.

Reasons why we’ve never heard of it before

Banks prefer you to put money in fixed deposits (FD), simply because the lock-up helps them to manage their capital better for lending purposes.

In addition, banks and fund managers don’t heavily promote MMF because these institutions earn lesser profit (lesser commission for bank teller as well) from MMFs. Management fee for a MMF ranges from 0.25% to 0.50% per annum, which is extremely low compared to other investment products that range from 1% to 2% per annum.

Pros and Cons of money market fund

Pros

1. Comparable rate with FD

2. Can withdraw anytime

3. Low management fee (ranges from 0.25% – 0.50% per annum)

Cons

1. No capital appreciation

2. Not PIDM protected (unlike FD)

3. Returns may vary as market and economic conditions change

How to invest?

There are plenty of options available in Malaysia.

1. StashAway Simple

StashAway Simple is a cash management portfolio which invests solely in Eastspring Investments Islamic Income Fund. Its projected return (net of all expenses and rebate) is 2.4%* per annum as advertised on their website (https://www.stashaway.my/simple).

One of the best things about StashAway Simple is that it provides the flexibility to transfer in and out, and there is no minimum or maximum balance required in this platform.

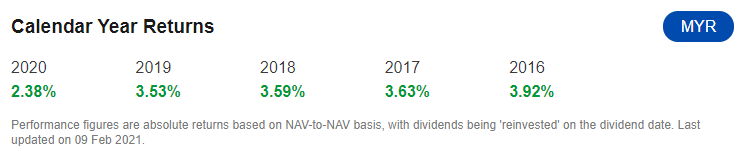

General information about Eastspring Investments Islamic Income Fund:

- Launch Date: 8 Feb 2007

- Fund Type: Income/Islamic money market

- Shariah compliant

- Top holdings as at 31 Aug 2020: Bank Islam Malaysia Bhd, Public Islamic Bank Bhd and RHB Islamic Bank Bhd

- Minimum initial investment if you wish to invest directly: RM50,000 (min subsequent investment: RM10,000)

- Annual management fee if you wish to invest directly: up to 0.25% p.a. of the NAV of the Fund

Performance return for Eastspring Investments Islamic Income Fund:

*I will discuss further on how they derived the 2.4% return and whether it is sustainable in my next post.

2. BIMB Dana Al-Fakhim

BIMB Dana Al-Fakhim Fund seeks to provide a regular stream of income by investing in Shariah-compliant short-term debentures, money market instruments and placement in short-term deposits.

General information about BIMB Dana Al-Fakhim

- Launch date: 27 Dec 2001

- Fund type: Income/Islamic money market

- Shariah compliant

- Top holdings as at 30 Nov 2020: Kuwait Finance House, Aj Rajhi Banking & Investment Corporation Bhd, Bank Islam Malaysia

- Minimum initial investment: RM1,000 (min subsequent investment: RM100)

- Annual management fee: 0.5% p.a. of the NAV of the Fund

Performance return for BIMB Dana Al-Fakhim:

3. Versa

Versa, a digital cash management platform newly launched on 29th Jan 2021 also provides opportunity to invest in MMF. It is launched in partnership with Affin Hwang Asset Management, the third largest asset management firm in Malaysia. Their projected return rate is 2.1% (information provided by Alex, Versa Customer Service Representative).

Similarly with StashAway Simple, they provide flexibility to withdraw funds anytime, though a minimum deposit amount of RM100 is required. Versa currently only allows deposit into one MMF which is the Affin Hwang Enhanced Deposit Fund.

It is nice to observe more competition arising in the fintech industry since the fight for retail capital is increasingly intensified (hopefully better rate or lower cost in future 😊).

General information about Enhanced Deposit Fund

- Launch date: 18 Apr 2005

- Fund type: Income

- Top holdings: Information not available

- Minimum initial investment if you wish to invest directly: RM10,000 (min subsequent investment: RM10,000)

- Annual management fee if you wish to invest directly: max 0.5% p.a. of the NAV of the Fund

Performance return for Enhanced Deposit Fund:

4. Fundsupermart (FSM)

Unlike the former 3 options, through FSM platform, you can easily personalize your investment into a variety of MMFs such as RHB Money Market Fund, Kenanga Islamic Money Market Fund, Nomura I-Cash Fund etc. It provides direct exposure to some funds, which simply only allows access to institutional and accredited investors.

However, I noticed that not all MMFs are available, e.g. Affin Hwang Enhanced Deposit Fund (Versa) is not within the fund selection in FSM. Further, there will be no sales charge or platform fee for money market funds in FSM.

(a) RHB Money Market Fund

General information about RHB Money Market Fund

- Launch date: 20 Jan 2006

- Fund type: Income

- Top holdings as at 30 Nov 2020: Sabah Dev Bank, Sabah Development Bank, Sunway Bhd

- Minimum initial investment: RM10,000 (min subsequent investment: RM5,000)

- Annual management fee: 0.5% p.a. of the NAV of the Fund

Performance return for RHB Money Market Fund

(b) Kenanga Islamic Money Market Fund

General information about Kenanga Islamic Money Market Fund

- Launch date: 9 Nov 2007

- Fund type: Income/Islamic money market

- Shariah compliant

- Top holdings as at 30 Nov 2020: CIMB Islamic Bank, Alliance Islamic Bank, MBSB Bank

- Minimum initial investment: RM1,000 (min subsequent investment: RM100)

- Annual management fee: 0.5% p.a. of the NAV of the Fund

Performance return for Kenanga Islamic Money Market Fund

(c) Nomura i-Cash Fund

General information about Nomura i-Cash Fund

- Launch date: 1 May 2019

- Fund type: Income/Islamic money market

- Shariah compliant

- Top holdings as at 31 Dec 2020: Ambank Islamic Bhd, Kuwait Finance House Bhd, CIMB Islamic Bank Bhd

- Minimum initial investment: RM10,000 (min subsequent investment: RM5,000)

- Annual management fee: 0.25% p.a. of the NAV of the Fund

Performance return for Nomura i-Cash Fund

So, which will I choose?

Let’s take a closer look on the comparison for their past performance in 2020.

*Breakdown of the rates obtained from Alex (Versa)

Based on the return rate above, it is pretty obvious that I would opt for StashAway Simple.

Other than the better rate of return, users of StashAway can also enjoy the following features which allows flexibility and convenience:

1. Easy registration through app or online

2. No minimum or maximum capped account balance

3. High flexibility to transfer in and out of portfolio (deposit 1 or 2 days: withdrawal 2 or 3 days)

4. No deposit requirement or withdrawal restriction

5. Projected rate of 2.4% (as at 9 Feb 2021)

What's ahead for the Malaysia economy?

By understanding what money market fund is, you will have an additional protection on your nest egg before inflation erodes the value of our nation’s currency. Of course, the 2.4% return from StashAway Simple barely nullify the inflation forecast above!

Hence for long term investment purpose, I strongly urge my readers to start investing and diversifying into the equity market after building up their emergency fund (~ 6 months’ worth of living expenses). Please also bear in mind that past performances of the above funds are not an indication of the funds’ future performances.

Definitely do your research before pooling your savings into any investment platform!

Disclaimer: I am neither an expert nor certified trader, and the views contained in this post should not be taken as an indication to buy or sell. I will not be held liable for any gains or losses incurred as a result of one's individual investing decisions after reading any post in this blog.

![[July 2021 Update] StashAway Simple is not that simple after all](https://static.wixstatic.com/media/d6c11b_9b1371a1676a464a836a040aea4a63d8~mv2.png/v1/fill/w_980,h_980,al_c,q_90,usm_0.66_1.00_0.01,enc_avif,quality_auto/d6c11b_9b1371a1676a464a836a040aea4a63d8~mv2.png)

Comments