Private Retirement Scheme: A complete guide to PRS and how I choose the best fund

- Hotcup

- Apr 24, 2021

- 8 min read

Updated: Apr 25, 2021

A few years back, my dad asked whether I would like to receive RM1,000 for free. I was like ???. “Just invest RM1,000 in PRS, and our government will top it up with another RM1,000”, he said. This is how I first started with my PRS investing journey without knowing what PRS is. 😅

Until 2021, when I first realized that I could enjoy up to a maximum of RM3,000 tax relief by contributing the same amount to my PRS fund annually, I started to throw myself with a lot of questions. Is it worth to contribute RM3,000 annually to this fund? Does it work the same as EPF or unit trust? What is the annual or sales fee? How were their past performances?

Here is what you should know about PRS 😊

Content:

1. What is PRS?

2. How PRS works

3. PRS tax incentive

4. What to consider when choosing a PRS?

5. How to select the best fund

6. How much should I contribute every month?

7. What if my PRS fund underperforms?

8. Is it compulsory to contribute every year?

9. I have an existing PRS fund. How do I invest into a different PRS fund?

10. When can I withdraw?

11. How do I get started?

1. What is PRS?

Private Retirement Scheme was launched in 2012 to complement EPF initiative. It is because most Malaysians do not have sufficient savings for retirement due to inflation, rising cost of living and healthcare costs.

PRS is similar to EPF. However, unlike EPF, PRS is a voluntary long-term retirement savings scheme which you can opt to contribute as little or as much as you prefer.

Besides, unlike EPF which is government-owned, PRS is privately run by financial institutions such as Public Mutual, Affin Hwang, Kenanga etc. With PRS, you are able to choose the PRS providers and their corresponding funds which you like to contribute.

You are also allowed to diversify your contribution into different PRS providers or funds. Each fund has different risk level and portfolio holdings. Confused? Don’t worry, I’m going to teach you step-by-step on how to make your fund selection below!

2. How PRS works

To start, you may choose to make contributions directly to the PPA portal, PRS Provider or through their registered distributors. Once you have successfully contributed into your PRS savings for the first time, you are automatically given a PRS account.

PPA, the central administrator for PRS will be administering your PRS account and will provide you with an annual consolidated statement of your PRS account with respective PRS Provider(s).

3. PRS tax incentive

Tax relief of up to RM3,000 per annum will be applied on individual taxable income for contributions made to the PRS from assessment year 2012 to 2025. Individuals may claim their tax relief for their PRS contribution under Section F-F18 of the BE Form.

The table below depicts the tax savings amount according to various income tax bracket when you contribute RM3,000 annually in PRS. For example, if your taxable income is between RM70,001 – RM100,000, your tax bracket is 21%. By contributing RM3,000 in PRS, you can enjoy tax savings of RM630!

4. What to consider when choosing a PRS?

a) Fee

Well, there is no free lunch in this world. Most of the financial products in the market come with charges $$. Below is the fee breakdown for PRS contribution via PPA.

i) Sales charge by transaction – 0.5% to 3%

ii) Annual management fee – 1% to 1.8%

iii) Annual scheme trustee fee – 0.04%

iv) Annual PPA administration fee – 0.04%

v) Transfer fee/switching fee etc

If you wish to know more on the fee details for any fund, you can always refer here. Just click on any PRS provider on the right panel. Under the “Fees & Charges” section, you would be able to find all details for any fees.

You can also refer here for fee comparison for all PRS providers.

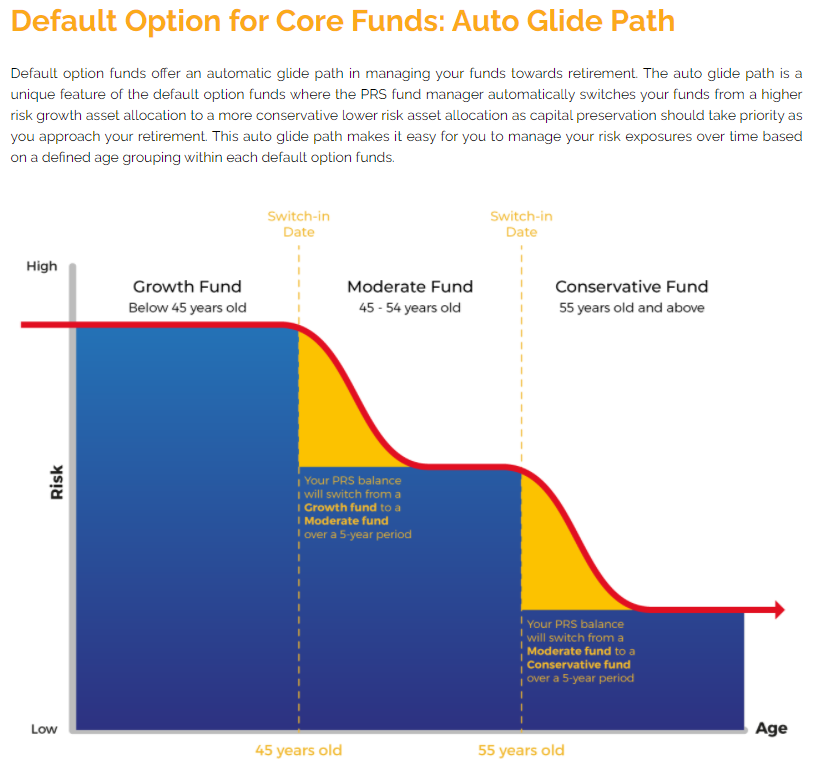

b) Risk tolerance

PRS providers are required by the Securities Commission to provide at least three “core” PRS funds, each with varying risk levels. Depending on your risk appetite and your age group, you can choose between Growth Fund, Moderate Fund or Conservative Fund. Besides, there are also other categories such as Non-Core and Non-Core Shariah.

Example below extracted from the complete list:

The main difference between core and non-core is that if you choose the core fund, you will be allocated to the following core funds based on your age grouping via the Auto-Glide Path. Alternatively, if you choose your own funds (self-selected option), you may choose any of the non-core funds based on your risk and return expectation.

c) Fund performance

PRS funds, like any other investment, do not guarantee returns. This means that your principal amount can fluctuate over time. Therefore, it is crucial to examine the performance of your funds regularly.

So, how should we evaluate the fund performance?

Shortlist a few peer funds to compare

It is difficult to assess the performance of a fund without comparing with its peers. PPA is being very helpful to actually list out the top 8 fund performers based on 5-Year and Year-to-Date performance. You can view it here under “Quick View” section. You may also get the complete list on all funds’ past performances here.

Focus on a longer time horizon for fund performance

Every fund comes with a disclaimer stating that the past performance is not reflective of future performance. However, the historical performance data can help us to scrutinize on how the fund performed across different economic conditions.

Any performance analysis should address a longer time horizon, e.g. 5 to 10 years since market and economic conditions played an important role influencing the performance of respective fund. For example, in the past 1 year, Islamic fund performance is relatively better due to the exclusion of the conventional banking, gaming, tobacco and alcohol sectors, which took a big hit during the pandemic.

Therefore, when assessing fund performance, it is better not to consider a short duration as the fund could possibly strengthen or weaken due to a one-off event. Remember, consistency can also shed light on the skill of the fund manager.

Understand and analyze the portfolio holdings

Other than looking at the returns of fund, it is also crucial to analyze where the fund manager has invested your hard-earned money. One of the easiest ways to understand the portfolio is to identify the top holdings and analyze the performance of these companies. Usually, the top holdings for the fund is stated in the Fund Fact Sheet.

Fund Fact Sheet is a document that gives an overview of a fund. It includes the fund objective, cumulative performance, calendar year returns, top 10 holdings, fees etc. It is a useful guide for new investors, especially before selecting and investing in a fund. You can just google or check it via Fundsupermart.

Example:

5. How to select the best fund

Step 1: Filter and select the top 5 funds

As of 31st March 2021, I’ve selected the top 5 funds based on their annualized return over the time horizon of 3 years, 5 years, 7 years and since inception.

Top 5 funds as of 31 Mar 2021:

AmPRS – Islamic Equity D

Principal PRS Plus Asia Pac Ex Jpn Eq A

Principal Islamic PRS Plus Asia Pac Ex Jpn Eq A

Public Mutual PRS Strategic Equity

Public Mutual PRS Islamic Strategic Equity

It turns out that Principal PRS Plus Asia Pac Ex Jpn Eq A is the best performance fund based on its annualized return. Its annualized return since inception (Nov 2012) is 12.74%, much higher than EPF and ASB*!

*Average return for EPF for the past 10 years is 6.11% while 7.94% for ASB Step 2: Understand the fund portfolio

Next, I drill down into their Fund Fact Sheets. For Principal PRS Plus Asia Pac Ex Jpn Eq A, it is the only fund in Malaysia that targets their investment in the Asia Pacific ex Japan region. The fund invests at least 95% of its NAV in a Target Fund - Principal Asia Pacific Dynamic Income Fund. I noticed the said fund has holdings in various established companies, such as Taiwan Semiconductor, Samsung Electronics, Tencent Holdings etc.

Step 3: Check the minimum contribution and its fee breakdown

As mentioned, under point 4(a), you may find all the relevant information below in the PPA website.

Principal PRS Plus Asia Pac Ex Jpn Eq

Step 4: Choose your best fund

Under Principal PRS Plus Asia Pac Ex Jpn Eq, as shown above, there are Class A, Class C and Class X. Class X is for institutional investor, and that leaves us with Class A and Class C. The differences between Class A and C are their fund size (personally I think this isn’t important as other factors), sales charge and annual management fee.

Assuming the annual return is at least 8% (since the fund has a target return of 8% per annum), if we invest RM3,000 annually in Class C, we would be able to get an end balance of RM264,191 in 30 years’ time, which will be slightly higher than Class A.

*Annual cost includes Management fee (1.4% for Class A; 1.5% for Class C), Trust fee (0.04%) and PPA Administration fee (0.04%)

6. How much should I contribute every month?

I would suggest only to take advantage of the maximum annual tax relief (i.e. RM 3,000), and definitely not to invest all free cash or savings into PRS funds. Reason being PRS has a very strict withdrawal policy, which withdrawal is only allowed after 55 years old.

7. What if my PRS fund underperforms?

PRS provides us the flexibility to switch our funds to another provider or fund, though there will be a switching fee (within same PRS provider) or transfer fee (other PRS providers’ fund).

8. Is it compulsory to contribute every year?

It is not compulsory to contribute every year. You may choose to top up or stop contributing any time you wish. There are no penalty charges.

9. I have an existing PRS fund. How do I invest into a different PRS fund?

You are only able to top up your existing PRS fund via PPA member portal. If you are interested to purchase a different PRS fund using PPA platform, you will need to process through their PRS online enrolment portal. The respective Provider may take up to 7 business days to confirm or reject the opening of the new PRS fund account.

10. When can I withdraw?

Contributions will be maintained in two separate sub-accounts as follows:

You are eligible to make full withdrawal upon reaching the age of 55. There will be a tax penalty of 8% imposed on pre-retirement withdrawals, which would be applied on the full withdrawn amount.

11. How do I get started?

One of the simplest ways is to sign up online and enrolled with PPA. Please refer file below for PPA’s step-by-step guide on its online enrolment process.

You may also sign up with Fundsupermart or respective PRS provider.

Hotcup’s Verdict

There are plenty of financial products in the market today such as Unit Trust or ASB. Some of them may outperform PRS funds. However, you are unable to enjoy the same tax relief if you invest in either Unit Trust or ASB.

For me, as long as I am able to enjoy the benefit of tax relief (not to mention tax saving could be re-invested), I will continue to top-up RM3,000 annually to this retirement fund. Remember to always research and compare before depositing your hard-earned money into any funds!

Disclosure: This article is not sponsored and solely for your reference only. Past performance is not an assurance of future results. I am neither an expert nor certified trader, and the views contained in this post should not be taken as an indication to buy or sell.

![[July 2021 Update] StashAway Simple is not that simple after all](https://static.wixstatic.com/media/d6c11b_9b1371a1676a464a836a040aea4a63d8~mv2.png/v1/fill/w_980,h_980,al_c,q_90,usm_0.66_1.00_0.01,enc_avif,quality_auto/d6c11b_9b1371a1676a464a836a040aea4a63d8~mv2.png)

Comments