Should you invest in Bauto?

- Hotcup

- Jun 6, 2020

- 4 min read

Updated: Dec 19, 2020

Bermaz Auto has finally launched their latest model Mazda CX-30 in FY2020. Ok, I gotta admit that I'm not a car person but it certainly looks really stylish and attractive. However, its price is more expensive compared to Honda HRV and Proton X70.

From an investor perspective, let's take a quick look on the past financial performance as well as the future growth of this company.

Mazda CX-30. Picture from https://www.caradvice.com.au/810492/2020-mazda-cx-30-pricing/

Bermaz Auto Bhd is engaged in the distribution and retailing of Mazda vehicles as well as providing after-sales services for Mazda vehicles in Malaysia and Philippines.

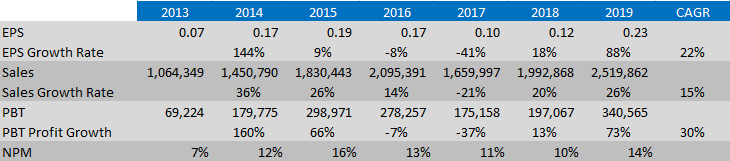

1. Increasing and consistent EPS

The increase in revenue was attributed by the growth of sales volume for CX-5 model from 16,517 units in FY2018 to 19,004 units in FY2019. The change in GST from 6% to 0% from Jun to Aug 2018 and the Group's offering to absorb SST for bookings received before 1 Sept 2018 also have boosted demand, in particular SUV models.

Bauto's EPS has grown rapidly over the past 7 years, achieving RM 0.23 per share in FY2019, which is more than THREEFOLD of its initial EPS (RM 0.07) in FY2013! Further, the consistent PBT growth (30%) is supported by the increasing revenue (15%) and increasing operating cash flow (29%).

2. ROE (>12%) and ROTA (>7%)

All investors like a company with high Return on Equity (ROE) and Return on Total Asset (ROTA). Over the last 7 years, Bauto has recorded an average ROE of 34% and ROTA of 20%. Its high % return indicates the business is of high quality, but the fact that this was achieved without leverage (see point 3) is truly impressive.

3. Low D/E ratio

The ideal debt over equity (D/E) ratio is preferably below 0.5. As at FY2019, Bauto has zero borrowing and its liabilities are mainly related to trade and other payables. However, based on Jan'20 announcement, the group has reported short-term borrowings of RM103mil which has resulted in the increase of D/E ratio to 1.18 for 1Q2020.

4. Does the company have long-range outlook in regards to profits?

(i) Future outlook

No doubt Covid-19 outbreak has resulted in devastating impact to the country’s automotive industry. Luckily, in Jun'20, the government allowed full exempt sales tax for locally assembled cars, and halved the sales tax for imported cars to 5% (from 10%) from 15 Jun to 31 Dec 2020.

The move was announced by Prime Minister Tan Sri Muhyiddin Yassin in his address to the nation today on the RM35bil Short-term Economic Recovery Plan. This will result in cheaper cars, and higher demand for cars from buyers wanting to capitalise on the tax holiday, which was seen when the previous GST was zero-rated for three months in 2018.

Currently, Bermaz has two CKD models; the CX-5 and CX-8, both locally-assembled at its joint venture company Mazda Malaysia’s assembly plant in Kulim. The latest model Mazda CX-30 is currently imported from Japan.

Bauto is negotiating to localize CX-30 to be started in the first half of 2021.

(ii) Expansion

Bauto has invested around RM20mil in the incremental capacity at 29% owned-associate Inokom (Kulim assembly plant), which Bauto will occupy 50% of the enlarged Inokom capacity, that is to say around 40,000 per annum, versus previous 28,000-30,000 per annum.

The capacity expansion is to cater to the localisation of two more models, which suspect to be the recently launched all-new CX-30 and the upcoming MX-30. As CX-30 is eligible for energy-efficient vehicle customized incentives, the success of localisation would significantly reduce its pricing.

Mazda's first mass-produced electric car - upcoming model MX-30

Picture from https://en.wikipedia.org/wiki/Mazda_MX-30

5. Share price trend

Share price is quite consistent across last few years, ranging from RM 2 to RM 2.5. However due to the Covid-19 impact, the price took a plunge in early 2020 to RM 1. As a value investor, I definitely see this as an opportunity for a bargain purchase. Currently share price has entered an uptrend recovery stage, which could be an excellent opportunity to stock up this share.

6. Conclusion: To buy or not to buy?

The automotive industry remains challenging and competitive as consumers are more careful with their discretionary spending.

Based on Jan'20 quarter report (3Q2020), the group's financial position remains healthy with net equity of RM479mil and positive net cash position of RM198mil despite short-term borrowings of RM103mil and dividend paid of RM32mil which declared in Feb 2020.

As a value investor, I would prefer to enter when the stock falls below its intrinsic value:

a) Fair value (include 33% margin of safety) = RM1.54

b) Discounted cash flow = RM6.21

c) Based on Earning method = RM0.86

*Intrinsic value is calculated based on my personal valuation

Again, past performance is not indicative of future performance. Do your homework before you invest!

Feel free to share with me your opinion below :)

Disclaimer: I am neither an expert nor certified trader, and the views contained in this post should not be taken as an indication to buy or sell. I will not be held liable for any gains or losses incurred as a result of one's individual investing decisions after reading this post.

Comments