REIT Analysis: AXIS REIT, IGB REIT and KIP REIT

- Hotcup

- Dec 19, 2020

- 7 min read

Today, Covid-19 has radically changed the outlook of the real estate sector. We can't deny that the impact of the pandemic has changed the consumer behaviors, attitudes and purchasing habits, and many of these will remain even after post-pandemic. People are spending more consciously and are embracing e-commerce.

With more people shopping online, the shopper traffic in retail and shopping malls has declined severely. While there is still uncertainty on the pandemic's long term impact, retail and hotels' performances are expected to rebound when vaccine is available.

As a result from the tremendous success in the global e-commerce sector, industrial REITs are being seen as a potential bright spot due to the surge in demand for logistics facilities catered for storage/sorting/distribution of shipping products. Big private equity players have actively added both industrial and data centre REITs into their portfolio, for example, Blackstone has made the biggest-ever purchase of an industrial real estate asset in China for $1.1B in Nov'20, whereas AXA has spent $880M to add Tokyo data centre and apartments into their Japan portfolio in Dec'20.

Despite market uncertainty, REITs are still one of the best long term dividend-stock investments. For today's topic, I have decided to analyze these 3 famous REITs (i.e. AXIS, IGB and KIP) because of their good fundamental.

1. Property type and its geographical location as at 30 Sept 2020

AXIS REIT

- Consists of 18 warehouse logistics, 18 manufacturing facilities, 13 office/industrial and 2 hypermarkets

- Johor Bahru (26%), Shah Alam (22%), Petaling Jaya (21%), Klang (9%) and other states (22%)

IGB REIT

- Consists of Mid Valley Megamall and The Gardens Mall

- Kuala Lumpur (100%)

KIP REIT

- Consists of 6 KIP Malls and 1 AEON

- Central region (3 KIP Malls), Southern region (3 KIP malls), Northern region (Aeon Mall Kinta City)

2. Net property income (NPI)

AXIS REIT has an average NPI growth of 8% per annum over the past 5 and 10 years. In contrast, IGB REIT has achieved a slower yet steady increase from 2016 to 2019 while KIP REIT's NPI has rocketed in 2020 which is due to the acquisition of AEON Mall Kinta City situated at Ipoh, Perak.

3. Number of properties

AXIS REIT has actively added manufacturing and warehouse facilities into their portfolio recently while IGB REIT has been maintaining only 2 retail malls in their property pool since its incorporation. For KIP REIT, other than the 6 KIP Malls, only 1 acquisition been made which is AEON Mall Kinta City as mentioned above.

4. Gearing ratio (Total borrowings / Total assets)

In 2020, Securities Commission Malaysia has temporarily increased the gearing limit for REIT to 60% in order to allow more flexibility in cash flow as well as debt and capital structure. While some REITs are struggling to maintain gearing limit, three REITs below are able to maintain a healthy gearing ratio below 40%. AXIS REIT has a slightly higher gearing ratio than the other two REITs, due to its recent acquisition on several properties.

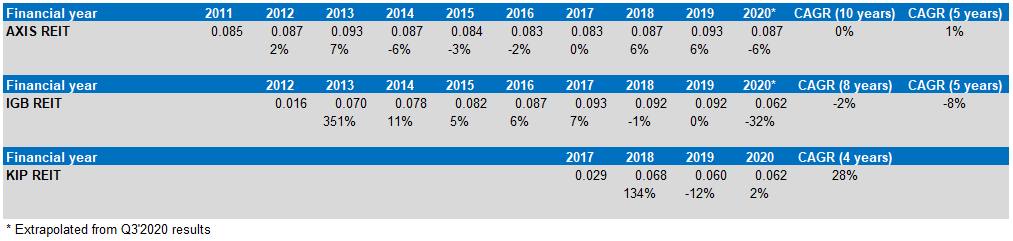

5. Distribution per unit (DPU)

For AXIS and IGB REIT, their CAGRs are not up to my expectation of an annual 5% increase in dividend pay-out. Despite KIP REIT's DPU has dipped in 2019, its performance should subject to more scrutiny since it is the most recent listed REIT in Bursa and is lacking of financial inputs.

6. Distribution yield (DPU/Share price)

A high distribution yield is one of the criteria to look for before investing in a REIT. As you can see, since KIP REIT has a lower share price, it has contributed a higher distribution yield compared to the other two REITs.

7. Average occupancy rate

Mid Valley Megamall and The Gardens owned by IGB REIT have successfully secured 99% occupancy over the years. KIP REIT has a lower occupancy rate compared to AXIS REIT but it has been improving gradually in last 3 years.

8. Net asset value (NAV) as at 30 Sept 2020

Currently, only KIP REIT is undervalued while AXIS and IGB REIT are overvalued based on their NAV.

AXIS REIT: RM1.48 (Current share price: RM2.06)

IGB REIT: RM1.07 (Current share price: RM1.75)

KIP REIT: RM1.01 (Current share price: RM0.81)

9. Risk and challenges

AXIS REIT

In respect to the expansion of property portfolio, AXIS REIT has done a decent job. The weighted average lease expiry is 6 years. However, it is noted that there are two tenants' businesses relating to the aerospace industry:

(i) Upeca Aerotech Sdn Bhd (lease period 20 years) - involved in manufacturing of aircraft parts and equipment

(ii) GKN Engine Systems Component Repair Sdn Bhd (lease period 6 years) - involved in servicing engine fan blades and fan discs for commercial aircraft

Due to the pandemic, aerospace sector has been experiencing lower demand as passengers stop travelling due to country border restriction. However as their lease expiry is more than 4 years, the risk of tenant drop out is lower and the deposit surrender upon rental default should be sufficient to mitigate any potential default risk.

IGB REIT

Since its incorporation, there is no further property acquisition apart from Mid Valley Megamall and The Gardens Mall. Management does not seems to have the intention to further acquire or expand their portfolio.

One possible scenario would probably be the future transfer of Mid Valley Southkey from sponsor (IGB) to the REIT portfolio. It seems that IGB REIT is acting as a cash cow for IGB operation as both businesses are under common director and management, hence there is no driving force on the management to further acquire or expand the REIT portfolio (other than via internal transfer).

The most significant risk for IGB is the current prolonged CMCO could cause tenants to drop out. To make matters worse for physical stores, many consumers may now prefer to shop online because of the pandemic, increasing challenges for the brick-and-mortar stores. However, with the availability of vaccine, I believe mall business will definitely recover in the long run as proven by the stable net property income and its consistently high occupancy rate.

KIP REIT

Unlike the big boys MNC and reputable regional retail stores, KIP malls target the communities of low and medium income groups, and therefore the tenants are mostly small businesses which provide basic necessities and essential services to the local community.

Its occupancy rate is gradually improving through the years (~2%) though still lower than my benchmark of 95%. Extracted from the recent 2020 annual report, there will be a total of 641 lease expiration with its tenants (also representing approx. 50.2% of total rental income) in financial year 2021. It is unknown whether these tenants are able to survive through the pandemic as shopper traffic is slowing down.

In addition, Covid-19 has accelerated the adoption of online grocery shopping due to community's Covid-19 concerns, its convenience and time savings. Based on a new study, online grocery is expected to double its market share by 2025, not to mention even during the post-pandemic period. However, 78% of shoppers would still prefer to visit a brick-and-mortar grocery store, indicating that most shoppers remain loyal to retailers with a physical store presence, according to the study.

Conclusion

AXIS REIT

Industrial REIT has been the recent highlight in the real estate sector as a result from the high demand of e-commerce. AXIS REIT was able to capitalize on the opportunity, coupled with its stable tenant base along with the future prospects, it is likely to thrive in today's market.

From point 2 above, we can see that the CAGR of its net property income is 8% over the past 5 to 10 years. The above-average earnings growth presents an attractive investment opportunity for the retail investors.

Besides, for industrial REITs, I like that tenants generally sign longer-term leases that include rental escalation clauses. The current market price is considered overvalued with a premium, hence dollar-cost averaging method will be highly recommended for interested investors like myself.

IGB REIT

Despite no expansion or acquisition over the years, IGB REIT is able to provide increasing DPU from 2012 to 2017 which is consistent with its NPI growth. However since 2017 onwards, its DPU has became stagnant in tandem with its NPI.

The performance of this retail REIT is solely depending on the positive rental reversion and increasing tenants' sales growth, as it seems that management has no immediate plan for any expansion or acquisition in the near future, other than some likelihood of bringing in Mid Valley Southkey into their existing portfolio as mentioned above.

Though in the absence of any acquisition, the two famous malls owned by IGB REIT have a strong competitive advantage due to its strategic location in the city of Kuala Lumpur, surrounded with offices and hotels. I personally love to shop in Mid Valley Megamall as they have a successful tenant mix which provides a wide range of merchandise and services.

KIP REIT

Despite the economy uncertainties and impact on consumer sentiments which may affect the portfolio's performance, I believe the shopper traffic at the malls will gradually improve with the availability of vaccine by 2021. Besides, KIP REIT's business nature which its tenants provide cheaper and affordable basic necessities for the community has became a competitive advantage since community now has become more cautious in spending and the culture of work from home has stimulated people to dine in at home.

In Oct'20, KIP REIT has announced that they will diversify its asset portfolio to include industrial and commercial real estates. A diversified portfolio would likely increase the investors' long term returns, coupled with lower risk.

For KIP REIT, I like its high distribution yield at an average of 7.8% (point 6) which is higher than both AXIS and IGB REIT. As long as they are able to secure tenants and provide high dividend yield in the long run, I can't see any reason to not invest in this undervalued REIT.

Disclaimer: I am neither an expert nor certified trader, and the views contained in this post should not be taken as an indication to buy or sell. I will not be held liable for any gains or losses incurred as a result of one's individual investing decisions after reading this post.

Comments