Case Study: Young Man Saved from Inflation

- Hotcup

- Aug 30, 2020

- 4 min read

Recently, I had come across a friend who faced the following problem:

“He is currently 24 years old, with RM30,000 savings. He does not have any personal liabilities or commitment. He previously had some experiences in investing stocks but was not able to generate much return from it. Further, due to his busy work schedule, he does not have time to monitor any stock or funds. Similarly, starting a business would be difficult for him as well due to his busy daily work routine from 9am to 7pm. Whereas during weekend, he prefers to take a break from work by resting and hanging out with friends. Nonetheless, he wishes to find a way to grow this fortune where time/risk/reward would be sustainable for his schedule in long run.”

To be honest, I am glad that he has the self-awareness that inflation is slowly chewing up our savings and I would say that it is never too late to start investing (also the number 1 solution to combat inflation!). However, there are many investing instruments to consider, such as fixed deposit, PRS, EPF, unit trusts, REITs, stocks, commodities, or even properties. Therefore, I would strongly advise anyone to take a few hours during the upcoming weekend to research on my following recommendation. After all, this is your money!!

1. Invest in high dividend yield stocks

For these stocks, their annual return from dividend could easily surpass our local fixed deposit rate, where most banks offer between 2% to 3.5% (as at August’20). I would personally recommend the following two classes of high yield stocks:

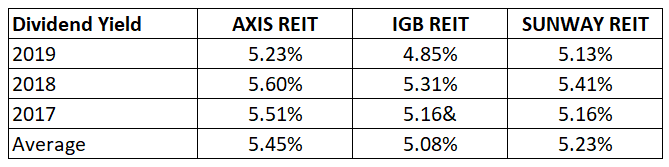

(a) REITs, are companies that own and collect rental from properties of various sectors, such as commercial, residential, hospitality etc. A few big players, which include Axis REIT, IGB REIT and Sunway REIT have done a decent job in combating economic inflation by providing relatively high dividend returns. Dividend yield for such REITs can be easily up to 5%.

Dividend yield = dividend/share price

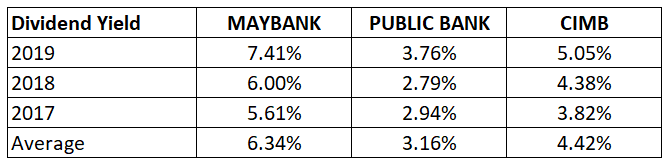

(b) Bank stocks such as Maybank and Public Bank are blue-chip stocks which also provide high dividend yield for their shareholders. Not to mention, these companies are generally more financially healthy and robust to changes in economic in comparison to growth stocks.

2. Invest in Exchange Traded Funds (ETF)

Unlike individual stocks, ETF holds a diversified basket of shares, bonds or other investment products. For example, one of the ETF in Malaysia, FBMKLCI easily provides their investors exposure to the 30 biggest listed companies which represent the Malaysian stock market. By investing in such ETF, retail investors will not need to get down to the nitty-gritty of researching any companies and diversification is already embedded in this investment vehicle.

We could also include international ETF in our portfolio since they will easily provide us with diversification beyond Malaysia market across different economies, currencies and offers growth potential of foreign companies.

Malaysia ETF is often not popular among investors due to its stagnant price since 2014. However, US ETF such as Vanguard S&P 500 ETF has a much better performance over the years compared to Malaysia’s ETF.

3. Dollar-Cost Averaging (DCA) strategy

Ever heard of dollar-cost averaging? It is an investing strategy where one would invest a fixed amount of fund across a period of time. The goal of dollar-cost averaging is to reduce the overall volatility impact on the purchase price of our investment since price is likely to vary each time one of the periodic investments is made.

I wouldn’t say that it is a standalone strategy, since it will be best to couple it with the above 2 recommendations. For such a case where a person has no commitment, I would suggest to put at least 50% of his monthly salary into these investment vehicles. Thereafter no brain work will be required, since all he needs to do every month, would be to transfer 50% of his pay check to his investment account and purchase the maximum number of shares that could be bought by the fixed monthly transfer.

I certainly think that robo-advisor is another decent option, though unlikely to generate significant gain in short term. For your information, robo-advisors are digital platform that provides automated investment services with little to no human supervision. Lower management fee is charged ranging between 0.2% to 0.8% annually compared to traditional banking products such as mutual funds which ranged between 1.25% to 5%.

We are considered as passive investors if we are investing through any robo-advisor as our portfolio will have a significant portion of index funds and ETFs. Yes, they are diversified, but that doesn’t mean that these genuine tools are able to beat the market in short term. Unless you have decided to invest for long term (at least 5 years or more), robo-advisor then may be your preferred choice.

Conclusion

Understand that at these uncertain times, when share prices fluctuate frequently, public tend to sell when price is soaring high and buy back at a lower price to benefit from the volatility. Some people may think that return from short-term trading is higher than long term passive investment. Perhaps they are indeed correct since they have been monitoring the market regularly and have properly done their research, but DID YOU?

If you have inadequate time to monitor price fluctuation or limited knowledge to analyse stocks, you should instead opt for passive investing strategy, where investing in high yield dividend shares or index funds is one of the simplest ways for a regular public to invest.

Comments