StashAway Simple is not that simple after all

- Hotcup

- Feb 20, 2021

- 7 min read

Updated: Jul 4, 2021

Is 2.4% return a marketing gimmick?

[July 2021 Update]: Please refer here for the updated article on the changes of the underlying fund in StashAway Simple on 18th June 2021.

After having some grasp on money market fund, I decided to take a deep dive into StashAway Simple for more information. Here is what I found.

Brief introduction

StashAway, the first licensed robo-advisor in Malaysia has launched its cash management fund - StashAway Simple on 15th June 2020.

With the introduction of StashAway Simple, retail investors have an alternative option of investing their short-term spare cash into money market funds (MMF). It appears to be an attractive investment as it generates comparable returns with normal bank fixed deposits (FD) and at the same time investors can enjoy the flexibility of cashing out their MMF investment anytime.

StashAway Simple is a cash management solution that pools investors’ money into Eastspring Investments Islamic Income Fund, with a rate of 2.4% (not guaranteed) as at Feb 2021. In the case of any changes in projected rate, they will provide an update correspondingly. Investors’ interest earned is accrued on a daily basis and paid out monthly.

Extracted from StashAway website:

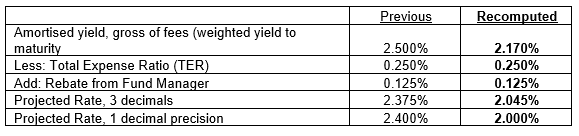

Their projected rate computation as at Feb 2021 is shown in image below. It is pretty straight-forward as the rate is based on the underlying fund’s weighted yield to maturity*.

*Weighted yield to maturity (WYTM) is the weighted average of speculative return rate/interest rate of a pool of investment, each having respective maturity period. WYTM is based on the belief or understanding that an investor purchases the investment at the current market price and holds until its maturity.

Recently, StashAway Singapore has lowered their projected interest rate for StashAway Simple from 1.9% to 1.4% from September 2020 onwards. The reason being is due to global central banks have been lowering interest rates to stimulate the economy.

It has led me to the question whether StashAway Malaysia is able to continue provide its attractive yield of 2.4% or are they lowering the projected rate anytime soon, following what StashAway Singapore did?

Besides, the benchmark interest rates in Malaysia are pretty low as well. As of Feb 2021, the latest KLIBOR 3-month and KLRR 3-month rates from BNM website are 1.94% and 2.02% respectively.

Next, let’s take a look on the details of its underlying fund - Eastspring Investments Islamic Income Fund.

How was the fund’s performance and how should we analyze it? Performance based on 1 year, 5 years or since inception?

Over a 5-year horizon, the total return is 18.51% which is an average of 3.7% p.a. whereas over a 1-year horizon, the return is much lower at 2.61%. The decrease is in line with the progressive decline of OPR from all-time high of 3.50% p.a. in 2008 to current record low of 1.75%. With the current economic conditions, will the interest rate progress to trend lower?

It is surprised that BNM maintained the OPR at 1.75% on Mar 2021 as it sees continued recovery in the global economy, although downside risks remain amid uncertainties around the Covid-19 pandemic.

With the current economic condition in Malaysia, the 2.61% return achieved in the past 1 year would be difficult to sustain in 2021.

So how much StashAway can actually achieve?

For the underlying fund, the latest average yield to maturity is 2.17% as of 31st Dec 2020 (2.29% - 30th Nov 2020). We can easily pluck in the figure above into the formula provided by StashAway.

Hence after subtracting the expense ratio of 0.25% and adding on the 0.125% rebate from fund manager, the net return derived is approximately 2% (instead of the projected rate of 2.4%). Assuming the current trend holds, the yield to maturity might potentially decline after first quarter of 2021.

Let’s hear from StashAway!

I’ve contacted StashAway to obtain further understanding on how they derived the average yield to maturity of 2.5%, and if any potential shortfall will be “topped up” by StashAway.

“So regardless of the returns from Eastspring itself, we set the projected rate to the value that we negotiated with Eastspring. You can consider it like an agreement that we agree on a rough value as we can’t guarantee the returns. If the yield from Eastspring is different than the returns in StashAway Simple, then yes we will definitely update the values, which was something that we did for the Singapore side.

We may also rebate an additional amount if the returns fall short of the projected rate at our discretion hence, it is not guaranteed per se.” – from StashAway

From the estimated projected rate, it seems like StashAway and Eastspring were expecting a higher return for both 2020 and 2021. Also noted that StashAway has full autonomy on whether to rebate the shortfall of the projected rate and hence the return is not guaranteed.

As of February 2021, we have yet to receive any update or announcement from StashAway on changes in its projected rate.

My actual experience with StashAway

To validate the current projected rate of 2.4%, we ran a pilot account with StashAway Simple for 1+ month. However, the result was disappointing (approx. 1.86% per annum), and again we consulted StashAway for an explanation:

“To clarify, the projected rate of 2.4% p.a. is the return figure earned per annum and you'll earn a return while your cash is invested on a daily basis (on a pro-rata basis). Having said that, the journey is not a linear line. For example, the dividends you earn monthly and rebates (paid out every quarter) would also play a significant role in your returns. Such that these additional funds will be reinvested into your portfolio resulting in a higher dividend payout and rebate amount down the road.” – from StashAway

Above statement clearly depicts that it would not be SIMPLE for retail investors to ascertain their returns, especially in cases with regular monthly deposit coupled with rebates that are only refunded on a quarterly basis.

As a user, I hope that StashAway are capable to present this in a clearer manner, since those returns are not guaranteed in any way. Further for more informed decision-making, they probably should explain in more detail on how projected rate would change and the key drivers for the change.

Are there any other better options?

Frankly speaking, the savings option are limited since I specifically prefer benefits which allow me to start with low minimum initial investment and the convenience to cash out anytime. Below are my recommendations.

1. OCBC 360 Account

OCBC 360 account allows you to enjoy up to 2.15% interest on your savings if you are able to fulfill all the pillars below. I think it is fairly simple to hit the first 3 pillars which comprise the base rate (0.05%), deposit pillar (0.70%) and pay pillar (0.70%, which is easily fulfilled by my default billings - phone bill, credit card bill and insurance payment).

For the spend pillar, it would be slightly difficult for myself as I don’t have a consistent monthly retail spending of RM500. Therefore, I always combine my spending with my partner in order for him to achieve the spend pillar. He will get the maximum 2.15% p.a. return whereas I will be earning only 1.45% p.a. (not as fantastic for myself so I would opt for option 2 below).

2. Frank by OCBC

For those similar like me who don’t spend more than RM500 a month, this is a better option as it allows you to earn an interest at 1.80% p.a. for money saved in the Save Pot (0.3% p.a. for money saved in Spend Pot). The minimum initial deposit is RM20. Further, there is no maximum balance, unlike OCBC 360 which its bonus interest is only accrued for the first RM100,000.

The difference between Save Pot and Spend Pot is distinct, as you could not withdraw or spend money in the Save Pot, unless you allocate them to the Spend Pot. You can easily allocate money from Save Pot to Spend Pot or vice versa anytime via their apps. The interest is accrued based on your account day-end balance (at 9pm) and will be paid out every month end. Sounds pretty simple and cool isn’t it? Especially for those who are looking for high interest savings account without the need to spend money.

3. Hong Leong Bank Pay&Save Account

From their website, it looks simple to enjoy up to 2.25% interest by fulfilling the 3 pillars below though it requires a higher deposit each month. Plus, there is an extra interest up to 0.9% p.a. when you invest via their share trading platform - HLeBroking.

However, after I dived further into their terms and conditions, there are some restrictions before you could achieve the advertised 2.25% + 0.9% return:

- To achieve Savings Interest of 1.25%, you are required to deposit at least RM2,000 in one sum monthly, hence might not be suitable for some with weekly wages; Further the 1.25% interest is only applicable on your first RM100,000 account balance.

- To achieve e-Xtra Interest of 0.50%, you must spend RM500 on online bill payments every month. This could be easy to achieve for those with monthly loan instalment.

- To achieve Bonus Interest of 0.50%, you must spend at least RM500 on your debit card on monthly basis (similar to OCBC 360’s Spend pillar).

- There’s a cap on both e-Xtra and Bonus interest at RM30 per month, hence only applicable on your first RM72,000 account balance.

- The extra interest of maximum 0.9% for share trading is only applicable for those who trade above RM100,000 each month, otherwise this will be irrelevant for most of us.

That’s why it is SUPER important to read terms and conditions before putting your money in any investment vehicle.

Conclusion

No doubt that StashAway has provided us with a simple MMF platform that could be easily managed by ourselves, and certainly it woud be a kindest surprise if StashAway continues to provide us with such a decent rate despite the drop in yield to maturity of the fund.

From the simple computation above, we believe the potential return should be closer to 2%. If StashAway opt to rebate additional amount in order to maintain its 2.4% return rate in 2021, it is clear that they wish to utilize the opportunity to promote their brand awareness while benefitting from the economies of scale. I believe there will be more intense competition to fight for capital in the future. Do your research before you invest!

Disclosure: The accuracy of the material found in this article cannot be guaranteed. Past performance is not an assurance of future results. I am neither an expert nor certified trader, and the views contained in this post should not be taken as an indication to buy or sell. This article is solely for reference only.

Comments